Consultation materials

This section was created for publishing documents issued by AECSD members and observers in order to provide consultations related to depository activities, new products and services, integration processes on the AECSD landscape, and to strengthen the cooperation with other regional associations.

By the authors’ request AECSD secretariat reviews submitted materials and publishes it in the Russian and English languages in case the materials are in compliance with the AECSD’s resolution and objectives.

Documents published in this section are not issued on behalf of the AECSD and represent personal opinions of the authors. Your comments and questions to the authors can be sent to the AECSD secretariat at aecsd@aecsd.com.

Sukuk — Islamic Bonds

Definition

SUKUK literally means contracts or promissory notes. In finance, it is an Islamic financial certificate which shares many attributes of a conventional bond but complies with Sharia principles.

Sharia is a set of Islamic religious law governing all aspects of daily life for Muslims. Sharia law provides Muslims with a set of principles and guidelines to help them make important decisions in their lives, such as finances and investments.

The issuer of SUKUK essentially sells an investor group a certificate and then uses the proceeds to purchase an asset that the investor group has direct partial ownership interest in. The issuer must also make a contractual promise to buy back the SUKUK at a future date at par value.

The pivotal features and functions of SUKUK are:

- An attractive means of financing

- A profitable investment

- An effective liquidity management strategy

- An efficacious risk management tool

- An appropriate method for fair wealth distribution

There are fundamental differences between SUKUK and conventional bonds as follows:

| Bond | SUKUK |

| Bonds have a fixed interest. | SUKUK are Sharia-compliant, avoiding Riba*. |

| Bonds indicate a debt obligation. | SUKUK indicate ownership of an asset. |

| The assets backing bonds may include products or services that are against Islam. | The assets that back SUKUK are Sharia-compliant. |

| Bond pricing is based on the credit rating of the issuer. | SUKUK are priced according to the value of the assets backing them. |

| Profits from bonds correspond to fixed interest, making them Riba. | SUKUK can increase in value when the assets increase in value. |

| The sale of bonds is the sale of debt. | The sale of SUKUK is the sale of the assets backing them. |

| The consumer is acting as the loaner and the bond issuer as a loan recipient. The loan has a fixed interest, therefore being Riba. | The purchaser is purchasing an asset that has value rather than participating in an implicit loan agreement. |

* Charged interest or usury

SUKUK Type

There are several types of SUKUK based on the functionality such as the parties’ purposes. The followings are the main kinds of SUKUK:

Not-for-profit

- Qardh al-hassanah (non-interest bearing): Benevolent and interest-free loan extended to people in need for a specified period of time. At maturity, the face value of the loan is to be paid off.

- Waqf (Endowment): An endowment of property to be held in trust and used for a charitable or religious purpose. It typically involves donating a building, land or other assets for religious or charitable purposes with no intention of reclaiming the assets.

Profitable Instruments

Profitable Instruments with Specified Rate of Return

- Murabaha: The seller and buyer agree to the cost and markup of an asset. It is an acceptable form of credit sale under Sharia.

- Ijarah: Lexically it means “leasing”. It is a leasing contract of property leased to a client for stream of rental and purchase payments, ending with a transfer of ownership to the lessee.

- Manfaat (Usufructs): A legal right accorded to a person or party that confers the temporary right to use and derive income or benefit from someone else's property.

- Istisna: A long-term contract whereby a party undertakes to manufacture, build or construct assets, with an obligation from the manufacturer or producer to deliver them to the customer upon completion.

- Salam: An advance payment for deferred delivery.

Profitable Instruments with Expected Rate of Return

- Musharekaha: A form of joint venture or partnership contract.

- Mudharabah: A profit sharing contract in which one party provides funds and the other management expertise.

- Muzaraah: An agreement between two parties in which one agrees to allow a portion of his land to be used by the other in return for a part of the produce of the land.

- Musaqat: A contract in which one party presents designated plants/ trees producing edible fruits to another party who undertakes irrigation in exchange for a common, defined share in the fruits.

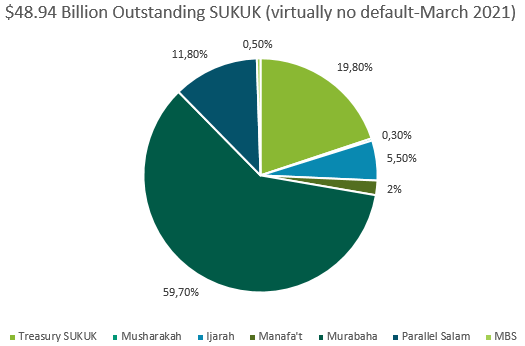

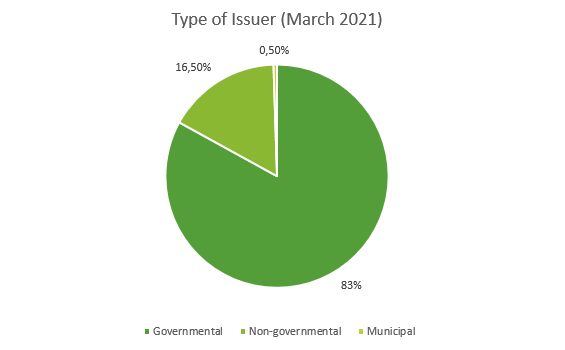

SUKUK in Iran

The following charts illustrate the data related to the SUKUK issuance in Iran by March 2021.

Role of CSDI

Central Securities Depository of Iran (CSDI) offers pre-trade and post-trade services to the Iranian capital market participants. CSDI was established as the sole registrar, safe-keeper, depository and clearing house for a broad range of financial instruments traded on the four Iranian exchanges i.e., Tehran Stock Exchange (TSE), Iran Mercantile Exchange (IME), Iran Energy Exchange (IRENEX) and Iran FaraBourse (IFB).

CSDI helps automate, centralize, standardize, and streamline processes required for the security and reliability of the market. It is in charge of the safe and efficient transfer of securities ownership and settlement of trade obligations.

CSDI is, first and foremost, to protect and mitigate risk for customers and investors. It plays a significant role in managing systemic risks facing the investors in the Iranian capital market. In terms of settlement risks, CSDI has a collateral management system in place that, among other responsibilities, provides sufficient liquidity for executing previously failed obligations.

CSDI is currently the parent company of one subsidiary and two associate companies, i.e., SAMAT Samaneh (99.97%), Capital Market Central Asset Management Company (49%), and Iran Financial Center (20%) that work aligned with CSDI’s core missions.

Established in August 2010, Capital Market Central Asset Management Company supervises and manages the establishment and management of SPVs in Iran’s capital market. It handles the entire logistical services for SPVs working as an investors’ trustee, preserving stockholders’ interests, assuring stockholders about issuer’s accurate performance, monitoring and controlling the securities (including SUKUK) issuance operation processes.

CSDI is present in the entire stages of the issuance, offering, clearing and settlement of the securities including SUKUK in the capital market. In the pre-trade stage, CSDI manages the entire work relatable to the registry and depository. It also manages the potential risks pertinent to its core functions. In the post-trade stage, it is in full charge of clearing and settlement of the transactions in the market.

CSDI is fully ready to share its experience in SUKUK market with its international counterparts, particularly, the members of AECSD. For further information or proposal of cooperation, please contact us at intl@csdiran.ir

Return to all news